Dollar Dominance 1945–2025: Gold, Nixon Shock, Petrodollar, and Global Trade

Introduction

Since the end of the Second World War, the U.S. dollar has reigned supreme as the backbone of global finance and trade. From the Bretton Woods Agreement in 1944, which tied currencies to the dollar and the dollar to gold, to President Nixon’s 1971 decision to sever that link, and finally the emergence of the petrodollar system, the dollar has dominated world trade and reserves.

This article traces the dollar’s journey from 1945 to 2025, explaining how America built its financial empire, why countries hold trillions in dollar reserves, and how global trade is still overwhelmingly conducted in dollars despite challenges from the euro, yuan, and other currencies.

1. Post–World War II: America’s Golden Loans to Allies

When World War II ended in 1945, Europe stood devastated. Cities lay in ruins, industries were destroyed, and millions of people faced hunger, poverty, and unemployment. The war had drained European economies of both resources and confidence. In contrast, the United States had emerged not only victorious but also economically stronger than ever before. Its industries had boomed during wartime production, and most importantly, it held the world’s largest gold reserves—nearly two-thirds of the global total. This unique position allowed the U.S. to take the lead in reshaping the postwar financial order.

One of the earliest steps in this process was America’s decision to provide large-scale financial assistance to its allies. These loans and aid packages were not just acts of generosity; they were strategic moves that helped establish the U.S. dollar as the foundation of the new global economic system. At that time, the dollar was still backed by gold at a fixed rate of $35 per ounce. This gold backing gave confidence to war-torn nations that American currency could be trusted, since it could always be exchanged for real, tangible wealth.

The Marshall Plan, officially known as the European Recovery Program, became the centerpiece of this effort. Initiated in 1948 and lasting until 1952, it directed over $13 billion into rebuilding Europe. Adjusted for inflation, that amount would be roughly $150 billion today. The money went into rebuilding infrastructure, revitalizing industries, stabilizing currencies, and securing essential supplies like food and fuel. Beyond financial aid, the Marshall Plan symbolized America’s commitment to preventing economic collapse in Europe—something that could have left the continent vulnerable to Soviet influence during the early stages of the Cold War.

By injecting dollars into European economies, the United States ensured that the currency became the preferred medium of international trade and finance. European governments and companies needed dollars to buy essential goods and raw materials, which in turn reinforced the habit of holding reserves in dollars rather than in local currencies. This demand for the U.S. dollar created a self-sustaining cycle of reliance: the more dollars circulated, the more indispensable the currency became in global trade.

The loans and gold-backed assurances were not just about economics—they also carried immense political significance. America positioned itself as the leader of the “free world,” building economic ties that would translate into long-term alliances through NATO and other institutions. The aid also gave the U.S. leverage in shaping the policies of recipient countries, aligning them with American interests.

In essence, the immediate post–World War II years marked the beginning of what historians call “dollar diplomacy.” Through loans, aid, and gold-backed confidence, the U.S. dollar established itself as more than just a national currency—it became the backbone of international trade. The Marshall Plan and other financial initiatives laid the groundwork for what would later become full-fledged global dollar dominance.

This period represents the first crucial step in a long journey: from gold-backed loans in the 1940s, to petrodollars in the 1970s, and finally, to the present system where the dollar remains the world’s most powerful reserve currency.

In July 1944, as World Wa

The Bretton Woods System (1944–1971)

r II was nearing its end, representatives from 44 Allied nations gathered at the Mount Washington Hotel in Bretton Woods, New Hampshire. Their mission was to design a new financial order that would prevent the kind of economic instability that had fueled the Great Depression and the rise of fascism in the 1930s.

The conference established a system in which all major world currencies were pegged to the U.S. dollar, and the dollar itself was directly tied to gold at a fixed price of $35 per ounce. This arrangement meant that the U.S. dollar became the anchor of the global economy. Other countries would hold dollars as their primary reserves, secure in the knowledge that those dollars could always be exchanged for gold.

To support this new structure, two key international institutions were created:

-

The International Monetary Fund (IMF): tasked with overseeing exchange rates, providing short-term financial assistance, and ensuring monetary stability.

-

The World Bank: focused on long-term development projects and reconstruction, particularly in war-ravaged Europe and Asia.

This system gave the United States extraordinary influence. Because the dollar was the central currency of trade and finance, demand for it surged. For nearly three decades, the Bretton Woods System brought relative stability to global markets, helping nations rebuild and fostering international trade.

However, the system also placed a heavy burden on the U.S. By the late 1960s, America’s gold reserves were insufficient to cover the vast amounts of dollars circulating abroad. Mounting deficits from the Vietnam War and domestic spending strained confidence, setting the stage for the eventual collapse of Bretton Woods in 1971 when President Nixon ended the gold-dollar link.

3. Cracks in Bretton Woods and France’s Gold Demand

By the early 1960s, the Bretton Woods system was beginning to show signs of strain. The United States, which had anchored the system with its promise to convert dollars into gold at a fixed rate of $35 per ounce, was spending heavily on two fronts: the costly Vietnam War and ambitious domestic programs under President Lyndon B. Johnson’s “Great Society.” These massive expenditures fueled inflation and led to growing doubts about whether the U.S. could maintain the dollar’s convertibility into gold.

Foreign governments began to notice that the volume of U.S. dollars circulating globally far exceeded the amount of gold in American reserves. Economists and policymakers called this situation the “dollar overhang”—a dangerous imbalance where America’s promises outweighed its actual gold holdings.

One of the sharpest critics of this system was French President Charles de Gaulle. In a famous 1965 speech, he denounced the Bretton Woods arrangement as an “exorbitant privilege” for the United States, pointing out that America could print unlimited dollars while other nations were forced to hold them as reserves. De Gaulle argued that this system unfairly allowed the U.S. to live beyond its means at the expense of others.

France backed its criticism with bold action. Rather than simply holding dollars, the French government demanded gold in exchange. French naval warships were dispatched to the United States to physically retrieve gold from the Federal Reserve and transport it back to Paris. This dramatic gesture shook confidence in the system and inspired other countries to consider similar demands.

These pressures revealed the structural weaknesses of Bretton Woods. By the end of the 1960s, speculation against the dollar intensified, and the world moved closer to the eventual collapse of the gold-dollar link in 1971.

4. The Nixon Shock of 1971 – End of the Gold Standard

On August 15, 1971, U.S. President Richard Nixon shocked the world by announcing that the United States would suspend the dollar’s convertibility into gold. This decision officially ended the Bretton Woods system, which had governed international finance since 1944.

The background to this decision lay in the mounting economic pressures of the 1960s. The U.S. had been running huge budget deficits due to the Vietnam War and expensive domestic programs under Lyndon B. Johnson’s “Great Society.” These expenditures created inflation and caused other nations to question whether the U.S. really had enough gold to back the enormous number of dollars circulating worldwide.

By 1971, America’s gold reserves had declined sharply, while countries like France and West Germany demanded gold in exchange for their growing dollar holdings. The system was under immense strain, and the U.S. risked losing its gold at an alarming pace. Nixon’s move—often called the “Nixon Shock”—was therefore both dramatic and necessary from Washington’s perspective.

The announcement effectively transformed the dollar into a fiat currency—backed not by a tangible commodity like gold, but by the full faith and credit of the U.S. government. Many economists and politicians at the time feared global financial instability, but instead the dollar’s role as the world’s dominant reserve currency actually strengthened. International trade, oil pricing, and global finance remained firmly tied to the dollar.

The Nixon Shock marked a turning point in global economics, ending the era of gold-backed money and ushering in a modern system where currencies float against one another. It also cemented America’s unique ability to issue the world’s primary currency, giving Washington unmatched influence over international trade and finance.

5. The Birth of the Petrodollar (1973–1974)

-

Context and Challenge

In the early 1970s, the U.S. found itself in a precarious economic and geopolitical position. The Vietnam War had drained financial resources, inflation was rising, and President Nixon had dealt a shocking blow in 1971 by suspending the gold convertibility of the dollar—effectively collapsing the Bretton Woods system. The dollar was no longer anchored by gold, and the U.S. urgently needed a new foundation to maintain the dollar’s global influence.Oil Crisis and the Strategic Pivot

In 1973, OPEC unleashed an oil embargo against countries supporting Israel during the Yom Kippur War, triggering a dramatic oil price hike—from roughly $3 to over $10 per barrel—ushering in one of the most destabilizing global oil shocks. The U.S. economy reeled from the twin shocks of inflation and energy shortages, and policymakers sought a way to stabilize both oil markets and the dollar simultaneously.The Creation of the Petrodollar System

In a bold strategic move, the U.S. crafted a deal with Saudi Arabia in 1974. In exchange for American military aid and weapons, Saudi Arabia agreed to price its oil exclusively in U.S. dollars—and invest those petrodollars back into U.S. Treasury securities. Though never formally announced, this secret arrangement laid the foundation for what became known as the petrodollar system.The ramifications were swift and profound: since OPEC controlled much of global oil supply, pricing oil in dollars forced all oil-importing nations—even those not dealing directly with Saudi Arabia—to secure U.S. dollars in order to purchase oil. This had the effect of creating perpetual global demand for the dollar, anchoring it firmly in world trade.

The Feedback Loop of Petrodollar Recycling

But it didn’t stop at pricing. Petrodollar recycling soon became key to the system, whereby oil-exporting nations reinvested their dollar earnings back into U.S. financial markets—especially government bonds—and into U.S. banks via eurodollar markets. This recycling helped finance U.S. deficits, fund military and economic engagement abroad, and maintained robust demand for the dollar.Solidifying Dollar Dominance

What began as a strategic U.S.–Saudi deal soon became a global standard. Other OPEC members followed suit, pricing their exports in dollars. Meanwhile, countries around the world stockpiled dollars in their reserves to ensure access to oil. The dollar wasn’t just a medium of exchange—it became the very lifeline of the global economy.Enduring Legacy

Over the ensuing decades, this petrodollar system reinforced the U.S. dollar’s supremacy as the world’s primary reserve currency. Central banks and governments—and even global traders—structurally depended on the dollar. Even as rivals like the euro or petroyuan enter discussions, the petrodollar framework remains deeply entrenched in the architecture of global trade and finance.

Summary

-

Why it happened: The breakdown of Bretton Woods and oil shocks prompted the need for a new anchor for the dollar.

-

What happened: A covert 1974 agreement tied oil sales to the dollar in exchange for U.S. military and financial support.

-

Impact: Artificially created global demand for dollars, fostering the petrodollar recycling loop.

-

Result: Cemented the dollar’s role as the dominant global currency—a legacy that endures today.

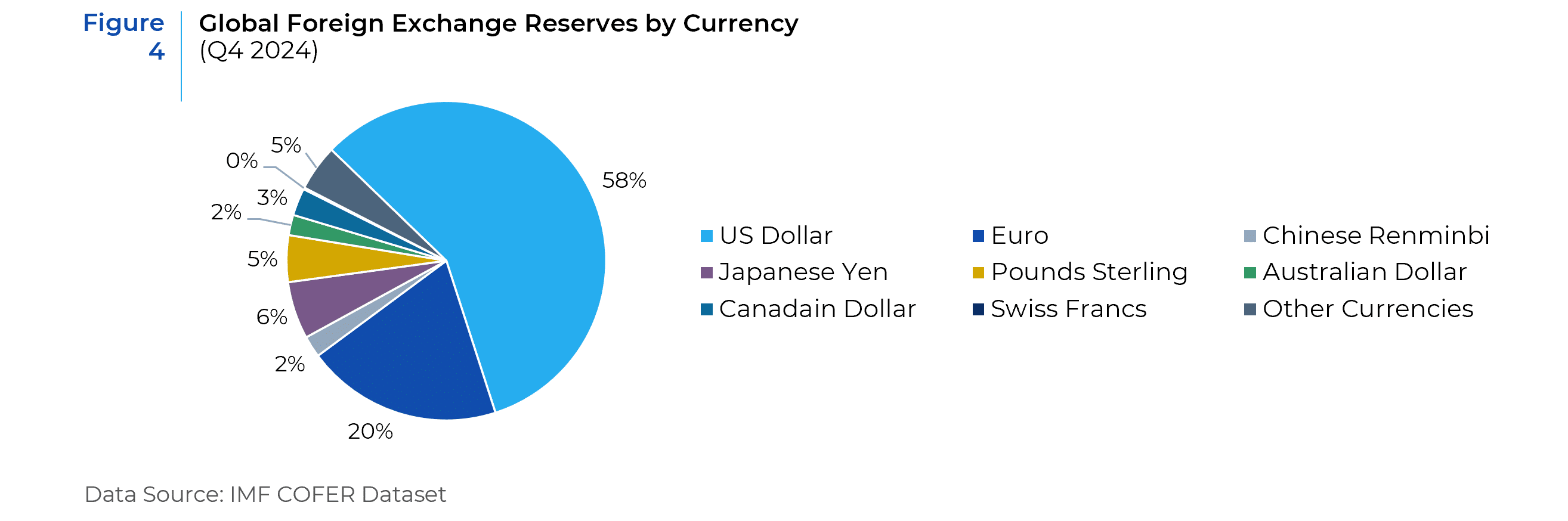

6. Dollar Reserves and Other Currencies

-

U.S. Dollar (≈58–60%)

The U.S. dollar remains the dominant global reserve currency, accounting for roughly 58% of official foreign exchange reserves in 2024. This continued strength underscores its trustworthiness, liquidity, and the deep and stable U.S. capital markets supporting it.

Euro (≈20%)

The euro holds the second-largest share at around 20%, reflecting its significant role in the European Union and global trade. However, structural issues like fragmented debt markets and the absence of a unified capital market limit its rise as an alternative reserve currency .

Japanese Yen (≈5–6%)

Taking up about 5% to 6% of reserves, the Japanese yen remains a minor but stable component. Its share aligns roughly with the scale of Japan’s economy and financial infrastructure.

Chinese Yuan/Renminbi (≈2–3%)

The Chinese currency now represents about 2% to 3% of global reserves—a modest rise from near zero a decade ago. While inclusion in the IMF’s SDR basket and China’s financial reforms help, capital account controls and limited convertibility continue to curb wider adoption.

British Pound (≈5%)

The pound sterling contributes around 5% of reserves. Its historical legacy and continued use in global finance help maintain its position, despite the UK’s relative decline in global economic influence.

Others

Remaining reserves are split among currencies like the Canadian and Australian dollars, Swiss franc, and increasingly gold—reflecting central banks’ diversification strategies in response to geopolitical and economic uncertainty.

7. U.S. Trade Dominance via the Dollar

The U.S. dollar serves not only as the cornerstone of global reserves but also as the predominant currency in international trade and finance—solidifying America’s economic influence.

Global Forex & Trade Invoicing

The dollar is ubiquitous in foreign exchange markets, involved in approximately 88% of all FX transactions in recent years. This dominance extends into trade: around 50%–55% of world trade is invoiced in dollars, even when U.S. involvement is absent.

Commodities and Pricing Power

Major commodities—such as oil, natural gas, and agricultural goods—are uniformly priced in dollars. This pricing standard reinforces the greenback’s indispensable role, compelling nations worldwide to maintain and transact in U.S. currency for basic economic operations.

Leverage Through Financial Infrastructure

Crucially, the U.S. exerts significant financial control via systems like SWIFT and dollar-clearing networks. By controlling access to these payment channels, Washington can impose powerful financial sanctions, effectively isolating targeted countries from global trade flows.

Why This Matters

-

Liquidity & Trust: U.S. capital markets offer unparalleled liquidity, making the dollar highly attractive for trade, reserves, and hedging.

-

Geopolitical Influence: The ability to restrict financial access gives the U.S. diplomatic and economic leverage.

-

Network Effects: Global institutions, businesses, and governments continuously rely on the dollar, reinforcing its network dominance.

In essence, the dollar’s role as the primary trade and clearing currency cements U.S. dominance. Whether through everyday transactions, strategic leverage, or commodity pricing, the greenback remains the linchpin of the global economy.

8. Top 10 Countries with the Largest Dollar Reserves (2024 estimates)

The countries with the largest dollar reserves maintain them to stabilize their currencies, support international trade, and ensure economic security. These reserves strengthen global confidence, provide financial resilience, and highlight the U.S. dollar’s enduring dominance in global markets.

| Rank | Country | USD Reserves (approx.) |

|---|---|---|

| 1 | China | $3.2 trillion |

| 2 | Japan | $1.2 trillion |

| 3 | Switzerland | $950 billion |

| 4 | Russia | $600 billion |

| 5 | Saudi Arabia | $500 billion |

| 6 | Taiwan | $460 billion |

| 7 | India | $450 billion |

| 8 | South Korea | $420 billion |

| 9 | Hong Kong | $410 billion |

| 10 | Brazil | $370 billion |

(Russia has diversified into gold and yuan after U.S. sanctions in 2022–23, but historically held large USD reserves.)

9. Dollar vs Other Currencies in World Trade

The dominance of the U.S. dollar in global trade and finance remains unmatched, despite increasing discussions around “de-dollarization.” The dollar continues to be the backbone of international reserves and transactions because of its deep liquidity, global acceptance, and the trust placed in the U.S. financial system.

As of recent data, the dollar accounts for roughly 58–60% of global foreign exchange reserves. More importantly, it is used in more than half of global trade, even in cases where the United States is not a direct party. This means countries trading with each other, such as Japan and South Korea or Brazil and India, often settle their transactions in U.S. dollars because it provides stability and predictability.

The euro stands as the second-most important currency, making up about 20% of reserves and around 30% of trade, especially within the European Union. However, its influence remains largely regional and has not translated into global dominance on the scale of the dollar.

China’s yuan (renminbi) has been promoted as a rising competitor, supported by Beijing’s efforts to internationalize the currency through trade agreements and initiatives like the Belt and Road. Currently, it makes up only about 3% of reserves and 7% of global trade, showing modest progress but still far behind the dollar.

The Japanese yen and the British pound each contribute about 5% in reserves and international usage. Both are considered stable but limited in global reach.

In conclusion, while alternative currencies are slowly expanding their role, none offer the same combination of liquidity, trust, institutional support, and financial infrastructure as the U.S. dollar. For now, the dollar remains the world’s undisputed trade and reserve currency.

10. Challenges to Dollar Dominance (2025 Outlook)

The U.S. dollar continues to hold the top spot in global trade and finance, but by 2025, several emerging trends have begun to chip away at its unrivaled supremacy. While its dominance is still intact, the global financial landscape is gradually shifting, raising questions about the future of the dollar-centered system.

One of the most significant developments is the steady rise of China’s yuan (renminbi). Although its share of global reserves remains small compared to the dollar, Beijing has been successful in promoting its use in bilateral trade, particularly with Russia, Africa, and parts of Asia. The Western sanctions imposed on Russia after the Ukraine conflict accelerated Moscow’s pivot to the yuan, giving China’s currency new momentum in energy and commodity trade.

At the same time, digital currencies and central bank digital currencies (CBDCs) are reshaping how money moves across borders. Countries such as China, India, and the European Union are experimenting with CBDCs, which could eventually reduce reliance on the dollar for clearing and settlement. While these systems are still in early stages, their long-term impact could be profound, especially if they become interoperable across economies.

Another key challenge comes from BRICS nations—Brazil, Russia, India, China, and South Africa. This bloc has actively discussed alternatives to dollar-based trade, even floating the idea of a joint currency or expanding the use of local currencies in cross-border settlements. These efforts, though fragmented, signal growing dissatisfaction with a system where Washington wields outsized influence through sanctions and dollar-clearing networks.

Still, despite these challenges, the dollar’s dominance endures. Its strength rests on over 80 years of trust, liquidity, and global infrastructure, making it difficult to replace quickly. The 2025 outlook suggests competition is rising, but the dollar remains the anchor of world trade. Read More:Martindox